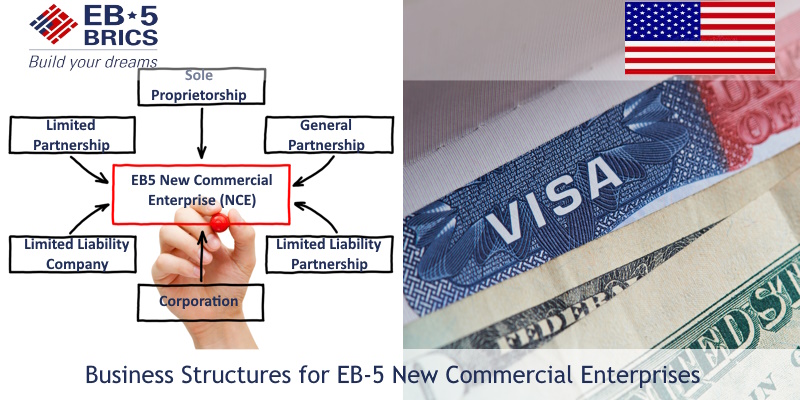

Business structures for EB-5 New Commercial Enterprises (NCEs) are forms of business entities that are acceptable for the EB-5 Visa Program. Business structures for EB-5 New Commercial Enterprises are commonly in the form of sole proprietorship, partnership, corporation, or limited liability company (LLC). An EB5 New Commercial Enterprise (NCE) structured as a sole proprietorship has a single owner and considers the business as the same entity as the EB5 Visa investor. Partnerships exist between 2 or more individuals or entities who agree to conduct business or trade activities together. An EB 5 NCE corporation is viewed as a separate entity from its owners and management and is afforded all the legal rights of an individual. A limited liability company (LLC) combines features of partnerships and corporations and is common for EB 5 New Commercial Enterprises.

Business structures for EB-5 New Commercial Enterprises (NCEs) are forms of business entities that are acceptable for the EB-5 Visa Program. Business structures for EB-5 New Commercial Enterprises are commonly in the form of sole proprietorship, partnership, corporation, or limited liability company (LLC). An EB5 New Commercial Enterprise (NCE) structured as a sole proprietorship has a single owner and considers the business as the same entity as the EB5 Visa investor. Partnerships exist between 2 or more individuals or entities who agree to conduct business or trade activities together. An EB 5 NCE corporation is viewed as a separate entity from its owners and management and is afforded all the legal rights of an individual. A limited liability company (LLC) combines features of partnerships and corporations and is common for EB 5 New Commercial Enterprises.

A New Commercial Enterprise must be a for-profit company that yields full-time positions to be qualified under the EB-5 Immigrant Investor Program. The number of jobs counted per immigrant investor depends on the type of EB-5 Project and the minimum capital required varies depending on the location of the NCE. The appropriate evaluation of an EB5 NCE Project should be conducted through thorough due diligence to ensure that the NCE meets the requirements of the EB 5 Program and that foreign investors achieve their immigration goals.

Table of Contents

What are Business Structures for EB-5 New Commercial Enterprises?

An EB-5 NCE can be structured into various types as long as the business activity results in profit and is conducted lawfully. EB 5 Visa investors should be knowledgeable about the acceptable business structures for an EB5 NCE to ensure the approval of their petitions and business plans. The next sections discuss the most common business structures for EB5 New Commercial Enterprises.

Sole Proprietorship

A sole proprietorship is a business entity that is owned by a single person or a married couple in certain instances. The sole proprietor owns all the assets and owes all liabilities of the business. A sole proprietor can operate on their own or hire employees. A sole proprietorship does not permit the owner to be a separate legal entity so the owner remains liable for business debts. The EB 5 Sole Proprietorship entity can be registered under the investor’s name or through a fictitious trade name.

Taxation of sole proprietorship businesses is included in the EB 5 investor’s personal income tax return (ITR) and U.S. Individual Income Tax Return filed through the Internal Service Revenue (IRS) Form 1040. The EB5 Visa investor’s adjusted gross income on Form 1040 is used as net income for ability to pay purposes but no tax forms list the NCE’s current assets and liabilities.

Partnership

A partnership is a relationship between 2 or more individuals or entities who agree to conduct business or trade activities together. Each individual or entity in the partnership contributes an essential component to the business such as capital, property, labor, or skill in return for a share in the profits and losses of the NCE. Each partner shares in the profits and losses equally or only partially depending on their investment or the agreement on the written partnership contract.

The Internal Service Revenue (IRS) typically views partnerships as pass-through tax entities which means that all of the partnership’s gains and losses pass through the company to the partners. The partners then pay taxes on their respective portions of the profits or deduct their respective portions of the losses on their individual income tax returns. As a result, the partnership does not pay income taxes on its own. Partnerships are still required to file the U.S. Return of Partnership Income (IRS Form 1065) to track whether the partners are reporting their income accurately.

The most common forms of partnerships for EB 5 New Commercial Enterprises are discussed below.

General Partnership

A general partnership is the most straightforward type of partnership and is often only termed a partnership. All partners or owners equally share responsibilities and liabilities in a general partnership EB 5 NCE.

These are the typical attributes of a general partnership EB5 business structure.

- Formed through an express or implied agreement.

- Consist of 2 or more partners.

- All partners or owners are liable for all legal actions and debts of the EB-5 New Commercial Enterprise.

Limited Partnership

A limited partnership is almost similar to a general partnership, however, the partnership is only partially owned by 1 or more limited partners and is exclusively operated by the general partners. Limited partnership businesses must always have at least 1 general partner with management power, the right to use partnership property, and is personally liable for the debts of the business. EB-5 Visa investors who are limited partners in a New Commercial Enterprise do not engage in managing the company and are only liable for business debts in relation to the amount they invested. A formal written agreement is necessary for limited partnerships to specify the limited liability and management ability of limited partners.

Limited Liability Partnership

A limited liability partnership (LLP) is a type of partnership wherein all partners have limited liability but without limitations on the management of the business. EB5 investors should look into the rules of the U.S. states if they plan to set up a limited liability partnership (LLP) as some states only permit professionals to use the LLP structure.

Limited Liability Limited Partnership

A limited liability limited partnership (LLLP) is similar to a limited partnership in that 1 or more limited partners and general partners are involved.

Here are the main characteristics of a limited liability limited partnership (LLLP).

- General partners operate the business while limited partners usually only maintain a passive financial interest.

- All partners have limited liability in the partnership.

- The organizational structure and allocation of profits and losses are decided by the partners.

A formal written partnership agreement is recommended by U.S. states for LLLPs though some states do not allow or recognize the LLLP business structure.

Corporation

A corporation is formed through the filing of articles of incorporation within a US State. A corporation is viewed as a separate entity from its owners and management and is afforded all the legal rights of an individual including the ability to bring and defend lawsuits and sell and purchase properties. An EB 5 NCE structured as a corporation is run by directors and officers and protects the owners (shareholders) from personal liability from debts and obligations.

Below are key features of a corporate business structure.

- Shareholders are able to transfer their stock to other individuals or entities if they choose to leave the corporation or in case of death.

- Shareholders own the corporation, the board of directors acts as managers and directors of the business, and officers supervise the daily operations of the NCE.

- Shareholders elect the members of the board who then appoint the officers.

- Smaller corporations typically have one individual perform the functions of a shareholder, director, and officer.

- Corporations must meet regularly to conduct formal decisions and meet annual reporting requirements in their state of incorporation and in the US States where they conduct substantial business activities.

The types of corporations that are valid for the EB-5 Immigrant Investor Visa Program are discussed below.

Subchapter C Corporations

A Subchapter C Corporation (C-corp) is a type of corporation wherein the owners or shareholders are taxed separately from the company. Double taxation exists in Subchapter C Corporations since the company is still subject to corporate income tax. The taxable profits of a C corporation are the money held in the business to cover its costs or expansion (retained earnings) as well as profits that are paid out as dividends to the owners (shareholders). The dividends are taxed twice due to the fact that the shareholders are also taxed on these dividends. C corporations are able to lower their taxable income by deducting most of their business expenses spent on the lawful pursuit of profit.

Personal Service Corporations

A personal service corporation is a type of corporation where the employee-owners are involved in executing personal services. Personal services are services executed in the law, engineering, architecture, consulting, accounting, performing arts, actuarial science, and health sectors. Part of the corporation’s stock must be owned by employees who are executing the personal services.

As a business entity, a personal service corporation must pay taxes on its profits. A flat tax based on the highest corporation tax rate is applicable to personal service corporations. Personal service corporations typically distribute their profits as salaries to their employee-shareholders due to the high tax rate. The employee-shareholders then deduct personal taxes from their salaries.

Limited Liability Company

A limited liability company (LLC) is a hybrid business structure that contains elements of partnerships and corporations. Limited liability companies (LLCs) were designed to allow business owners to have liability protection without double taxation. The profits and losses of an LLC are passed onto owners and are included in their personal tax returns. The LLC structure is common for EB 5 New Commercial Enterprises along with limited partnerships.

LLCs can either be handled by each of their members or by a designated manager who may or may not be a member of the LLC. The operating agreement for the LLC states the distinction between members and managing members. Managing members of the LLC are given full participation rights in running the NCE if such a distinction is recognized. Depending on the operating agreement, even regular members could participate in running the LLC. Limited liability companies can be dissolved after a specific period of time under conditions such as the death or exit of a member.

What is a New Commercial Enterprise?

A New Commercial Enterprise (NCE) is a business entity established through capital from immigrant investors designed to reap profits and create jobs. An New Commercial Enterprise must generally be formed after November 29, 1990 and lawfully conduct ongoing business. EB5 New Commercial Enterprises (NCEs) that were established on or before November 29, 1990 are qualified for the EB5 Visa Program if any of the following criteria are met.

- The existing business was purchased and restructured or reorganized to form an NCE.

- The business was expanded through EB 5 investment and a 40% growth resulted through a net worth increase or the addition of new employees.

The EB5 Visa Program is an immigration path for foreign nationals and their dependents seeking to obtain US Permanent Residency through investment. Investing in an NCE is one of the key requirements to qualify for the USA EB5 Investor Visa.

How Does an EB-5 New Commercial Enterprise Work?

An EB 5 New Commercial Enterprise is set up through direct investment or through a regional center. A Direct EB-5 New Commercial Enterprise is an investment project that requires the active participation of the EB-5 Visa investor in the management and operation of the business. Direct EB5 Projects must yield jobs directly from the operations of the business itself. A Regional Center is a public or private entity assigned by U.S. Citizenship and Immigration Services (USCIS) to boost economic growth. EB 5 Regional Centers pool funds from multiple immigrant investors to finance commercial projects. Indirect and induced jobs resulting from the positive economic impact of Regional Center Projects are counted towards the job creation requirement of the EB-5 Visa Program.

What are the Requirements for an EB-5 New Commercial Enterprise Investment?

EB5 New Commercial Enterprises must meet key requirements to be qualified projects under the EB-5 Visa Program regardless of the business structure. These requirements are also the main criteria for immigrant investors who wish to gain USA Permanent Resident status.

Capital Investment

The EB5 capital investment is cash and all real, personal, or mixed tangible assets of the immigrant investor.

The following are not qualified for EB5 Visa capital investments in a New Commercial Enterprise.

- Assets obtained directly or indirectly from unlawful activities.

- Investment made in exchange for a note, bond, convertible debt, obligation, or other types of debt contract between the immigrant investor and EB 5 NCE.

- Capital invested with a guaranteed rate of return from the EB-5 New Commercial Enterprise.

- Invested capital that is subject to any agreement between the immigrant investor and the EB5 NCE that grants the investor a legal right to repayment, with the exception that the new commercial enterprise can have a buyback option that can be exercised solely at the NCE’s discretion.

The minimum capital investment varies depending on the location of the EB 5 New Commercial Enterprise. Investors in EB-5 New Commercial Enterprises located in Targeted Employment Areas (TEAs) must invest a minimum of $800,000 USD. A Targeted Employment Area (TEA) is located in a rural area or a high unemployment area. Investments in EB5 NCEs located outside a TEA must be at least $1.05 million USD.

Job Creation

The EB-5 NCE is required to create jobs from the investments of immigrant investors. A minimum of 10 full-time permanent jobs must result from the capital of each EB5 Visa investor. Full-time employment means a minimum of 35 working hours per week for each qualified US worker. Qualified U.S. workers are US citizens, lawful permanent residents (LPRs), conditional residents, temporary residents, asylees, refugees, and persons living in the USA under suspension of deportation. The EB 5 Visa investor, their spouses, and their children are not considered in the required minimum job count.

Direct EB-5 New Commercial Enterprises are only able to count the direct full-time employees of the business or its subsidiaries. EB5 New Commercial Enterprises under Regional Centers are able to count direct, indirect, and induced jobs. EB 5 investors in troubled businesses are able to rely on the maintenance of jobs of the existing employees and should not be less than the pre-investment level for at least 2 years. Check our complete guide on EB5 Job Creation rules and requirements.

How to Choose an EB-5 New Commercial Enterprise Project?

Choosing an EB5 New Commercial Enterprise Project requires conducting due diligence. EB 5 Project Due Diligence is the process of evaluating EB 5 NCEs, including their business structures, to help immigrant investors choose the most suitable investment.

Here are the important factors to consider when Choosing an EB5 Project.

- The EB-5 NCE industry. Certain NCEs are preferable for EB5 Visa investments due to their job-creating capacities such as hotels, restaurants, and real estate developments.

- The location of the EB5 NCE. The required minimum investment is based on the location of the EB-5 New Commercial Enterprise.

- The EB 5 Project classification. The management and job creation requirements differ for NCEs under direct and regional center projects.

- The job-creating capacity of the New Commercial Enterprise. The 10 full-time jobs must be created and maintained for at least 2 years after the EB 5 Visa investor puts their capital in the NCE.

- The return on investment from the EB-5 NCE. Investors should look into the history of EB-5 Project Developers and Regional Centers in terms of capital repayment.

- The repayment terms. The EB5 capital investment must remain with the NCE for at least 2 years or until the filing of Form I-829 (Petition by Investor to Remove Conditions on Permanent Resident Status).

- The capital stack. Capital stack refers to the types of capital or funding invested in the EB-5 Project. The different types of investment in a capital stack have different levels of risks and returns and also vary depending on the business structure of the EB 5 New Commercial Enterprise.

- The exit strategy. The EB 5 exit strategy is the plan that outlines how financial assets will be liquidated or tangible financial assets will be sold when specified conditions have been fulfilled or exceeded.

What is the Best EB-5 New Commercial Enterprise to Invest In?

The best EB-5 New Commercial Enterprise Projects for immigrant investors are the restaurant, hotel, real estate, and biotechnology industries. These EB5 Projects are the ideal NCEs for completing the program’s job requirements for permanent residency. Our page on the Best EB5 Projects contains more information to help you choose the most suitable EB5 business to invest in.

Is a Non-Profit Organization a Qualified EB-5 New Commercial Enterprise?

No, a Non-Profit Organization (NPO) is not appropriate for EB 5 as New Commercial Enterprises must involve “for-profit” activities. A Non-Profit Organization (NPO) is typically involved in charitable, educational, religious, or artistic activities and profits are not distributed to the owners but go back to the organization. Restructuring the NPO to include for-profit activities can be done with the help of professionals such as an EB-5 Visa Attorney, EB-5 Economist, and financial advisor to qualify for the EB 5 Program.

Does a Subchapter S Corporation Work for an EB-5 New Commerical Enterprise?

No, a Subchapter S Corporation (S Corp) will not work for an EB5 NCE since this type of business structure does not allow ownership from foreign investors. A Subchapter S Corporation is a variation of a C-corp with the benefits of partnership taxation and limited liability protection. Consider other business structures such as a C-corporation, limited liability company, or limited liability partnership for your EB 5 NCE.

Can a Troubled Business Qualify as an EB-5 New Commercial Investment?

Yes, investing in a troubled business is a qualified New Commercial Enterprise for EB-5. A troubled business is a commercial entity that has been established for at least 2 years and has experienced a net loss during the 12 to 24 months preceding the immigrant investor’s EB-5 petition priority date. The loss must be at least 25% of the troubled business’ net worth before the loss.

Do I Need to Include the Business Structure of the EB-5 New Commercial Enterprise in My Business Plan?

Yes, the business structure and analysis of the NCE you invested in must be specified and explained in your EB5 Business Plan. A Business Plan for an EB-5 Visa investment is an important document submitted together with your Form I-526 (Immigrant Petition by Standalone Investor)/ Form I-526E (Immigrant Petition by Regional Center Investor). Your Business Plan for EB5 Visa demonstrates your capacity to invest the required minimum capital which yields jobs for US workers. A sound Business Plan that fits the EB 5 Program requirements increases your chances of obtaining a Green Card for US permanent residency.

Which Visa Holders are Eligible to Invest in an EB-5 New Commercial Enterprise?

Certain Nonimmigrant US Visa holders who are present in the United States are eligible to invest in an EB5 New Commerical Enterprise to obtain Permanent Residency (Green Card). A nonimmigrant visa is a stamp on the passport of foreign nationals that allows temporary residence in the US. Nonimmigrant visas with dual intent in particular are able to apply for the EB-5 Immigrant Visa without violating the conditions of their visa. Dual intent allows certain nonimmigrant visa holders to apply for US Permanent Residence legally.

Here are examples of dual intent nonimmigrant visa holders that are qualified to invest in an EB 5 NCE Project.

- H-1B Visa for specialty occupation workers.

- L-1 Visa for intracompany transferee managers and executives of global companies.

- O-1 Visa for individuals with extraordinary abilities and achievements in sciences, arts, education, business, or athletics.

- E-2 Visa for foreign investors from countries with treaties of commerce and navigation with the US.

Is an EB-5 New Commercial Enterprise Investment Risky?

Yes, the investment in a New Commercial Enterprise must be at risk for you to qualify for the EB 5 Visa as per U.S. Citizenship and Immigration Services (USCIS). The EB-5 NCE Project Investment must remain at risk until the I-829 petition filing to demonstrate that you meet the job creation and minimum investment requirements of the EB 5 Program. An at-risk EB-5 NCE investment means that the capital is subject to both gains and losses within the required period of investment.